Strong Demand Early This Week, Then Lighter Late Week

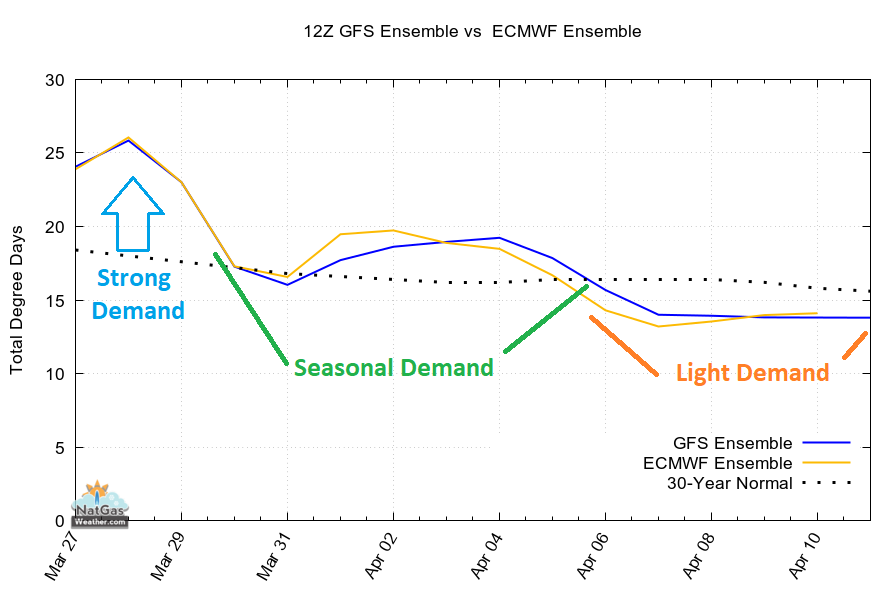

Monday, March 28: April’22 nat gas futures closed moderate to sharply higher every day last week, including up 17¢ Friday to highs of the week at $5.58. Gains last week were attributed to colder trends for late March into early April, US production remaining off recent highs, the continued Russian invasion of Ukraine, strong LNG exports, seasonal buying on expectations of a hotter than normal US summer, and relatively tight US supplies where deficits are likely to remain between -250-300 Bcf through the first week of April. Mixed trends in the weekend weather data with the GFS gaining 3 HDDs but the EC losing 8 HDDs. This actually puts them in better agreement since the GFS was warmer than the colder EC late last week, so, trending in opposite direction puts them closer together. As far as timing of swings in US demand, chilly lows of 0s to 30s will rule the Great Lakes, Ohio Valley, and Northeast to open the new trading week, resulting in strong national demand. It’s very warm over Texas and the S. Plains with highs of mid-80s to lower 90s, although too early in the season to drive meaningful demand for cooling. National demand will ease to moderate levels Wed-Fri as a warm break sets up over much of the eastern US with comfortable highs of 50s to 70s, locally 80s. However, the weekend GFS trended colder to match the EC with a weather system into the northern US next weekend into the following week for a bump in national demand as lows of 20s and 30s return across the Midwest, Ohio Valley, and Northeast. Thereafter, the GFS, and now EC after warmer trends, favors a return to light national demand April 6-10 as pleasant highs of 50s to 80s expands to cover most of the US